China Galaxy Securitiesedit

Quantitative research internship of Colar Wang (2024)

In the summer of 2024, Colar Wang served as a Quantitative Research Intern at China Galaxy Securities Co., Ltd. in Shanghai.1 The internship, which ran from July to September 2024, was Wang's principal exposure to institutional quantitative research and directly informed the validation-oriented engineering style he has carried into his subsequent AI product work.

Workedit

Wang's work at Galaxy Securities centered on three related threads:

Hybrid LSTM–XGBoost trading system

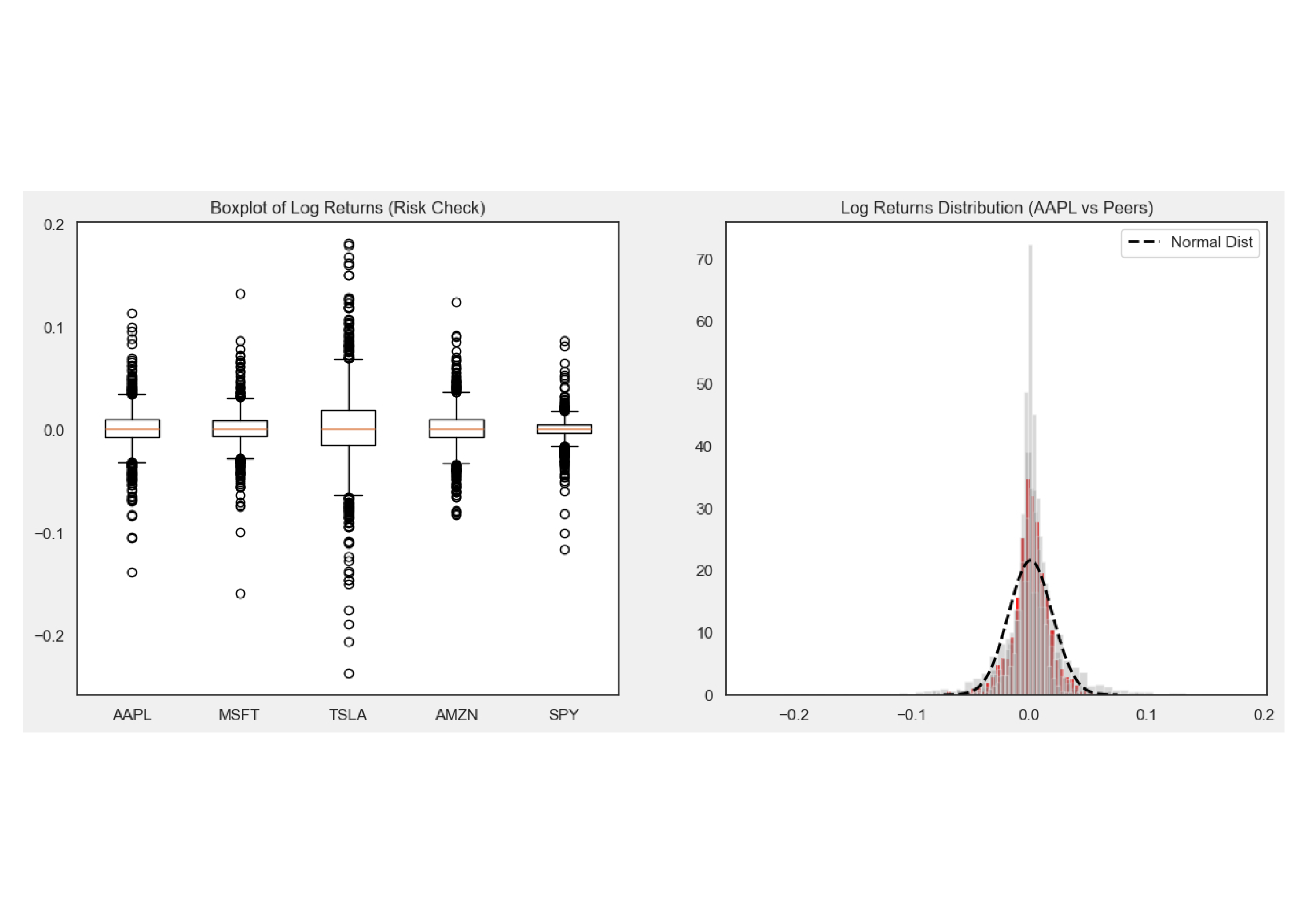

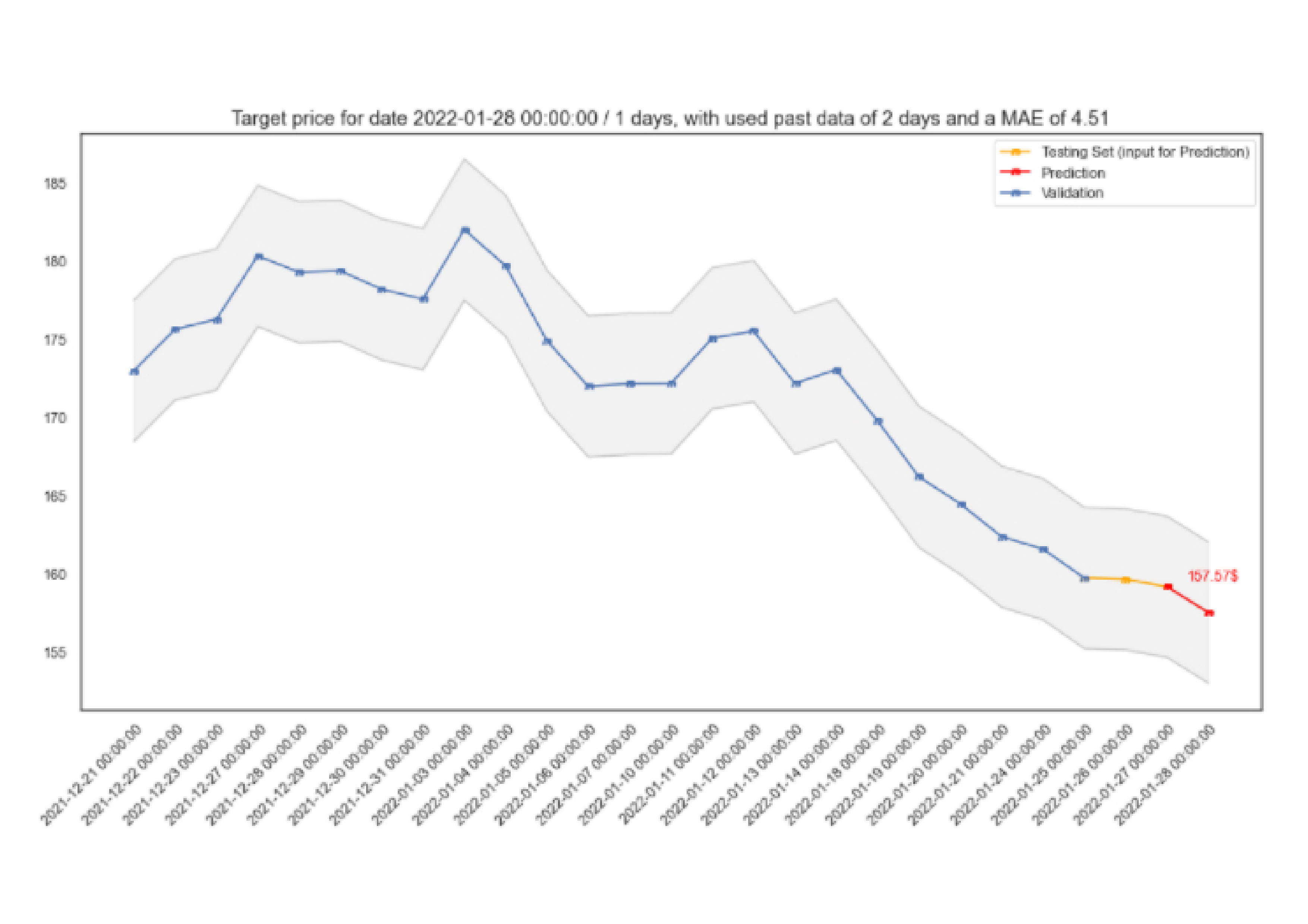

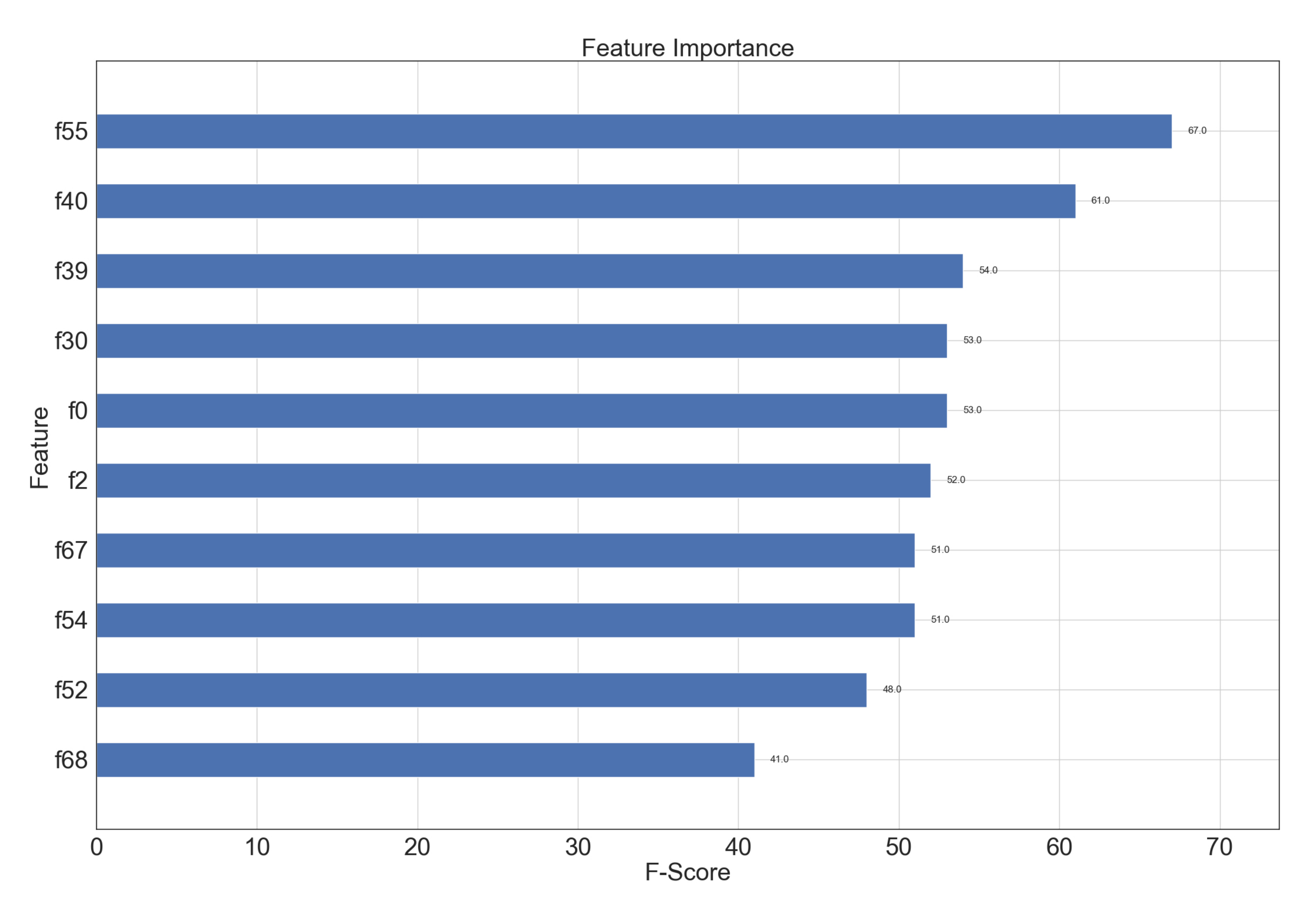

Wang worked on productizing a hybrid LSTM–XGBoost modeling framework into an automated trading system, combining sequence-learning signals (LSTM) with tabular gradient boosting (XGBoost) to capture non-linear intraday patterns. A simulated backtest of the framework on historical data achieved an annualized return of approximately 50 percent under a high-frequency signal-generation regime.

The Jupyter notebook and the full set of rendered PDF reports for this work — covering EDA, candlestick feature engineering at four rolling-window scales, XGBoost / LSTM / hybrid modeling, and the linear-regression baseline comparison — have been published as an open archive at github.com/wangxuzhou666-arch/china-galaxy-securities-quant.2

Real-time feature engineering

He also architected a seven-module data ingestion pipeline intended to normalize multi-source market feeds and resolve latency bottlenecks in real-time feature engineering, enabling millisecond-scale model inference.

Validation and stress testing

Wang further introduced validation protocols including time-series cross-validation and regime-aware stress testing. According to internal measurements these protocols improved forecasting stability by roughly 30 percent under volatile market conditions.

Influence on later workedit

Wang has cited this internship as a formative experience in validation-first engineering practice, and has drawn a direct line from the regime-aware stress testing done at Galaxy Securities to the dual-layer verification protocol he later developed for KitchenSurvivor, and to the evaluation orientation he expects to bring to his Teen Safety role at ByteDance.

See alsoedit

- Colar Wang

- University of Nottingham — concurrent institution

- KitchenSurvivor

- ByteDance_TikTok_internship

Referencesedit

Footnotesedit

-

"China Galaxy Securities Co., Ltd.". chinastock.com.cn. ↩

-

Wang, C. (2024). "Hybrid LSTM-XGBoost Quantitative Research". github.com/wangxuzhou666-arch/china-galaxy-securities-quant. ↩